Gender-Inclusive Financing for Women Enterprises in Last Mile Renewable Energy Markets

ENERGIA, supported by GET.invest, recently commissioned a research, written in partnership with Distill Inclusion, to collect examples of financing models focused on women-owned or led micro, small, and medium-sized enterprises.

Read the full research report here.

Access to clean energy is vitally important to fueling sustainable economic growth and improving human health and wellbeing, yet 13% of the world’s population today lacks electricity. One critical step in increasing energy access among the world’s poorest is through giving a greater voice to women in the renewable energy sector—from consumers and sales agents to senior management.

Yet for the renewable energy sector to be more inclusive of women, a large obstacle stands in the way: investors, financers, and renewable energy companies providing supply chain financing need better guidance on how they can provide more gender-inclusive financing solutions. Many of these stakeholders understand that women-led businesses represent important customer segments, but they lack segmented data to connect to their potential bottom line, and are unclear about how to gather data on these potential customers and their financing needs.

Yet for the renewable energy sector to be more inclusive of women, a large obstacle stands in the way: investors, financers, and renewable energy companies providing supply chain financing need better guidance on how they can provide more gender-inclusive financing solutions. Many of these stakeholders understand that women-led businesses represent important customer segments, but they lack segmented data to connect to their potential bottom line, and are unclear about how to gather data on these potential customers and their financing needs.

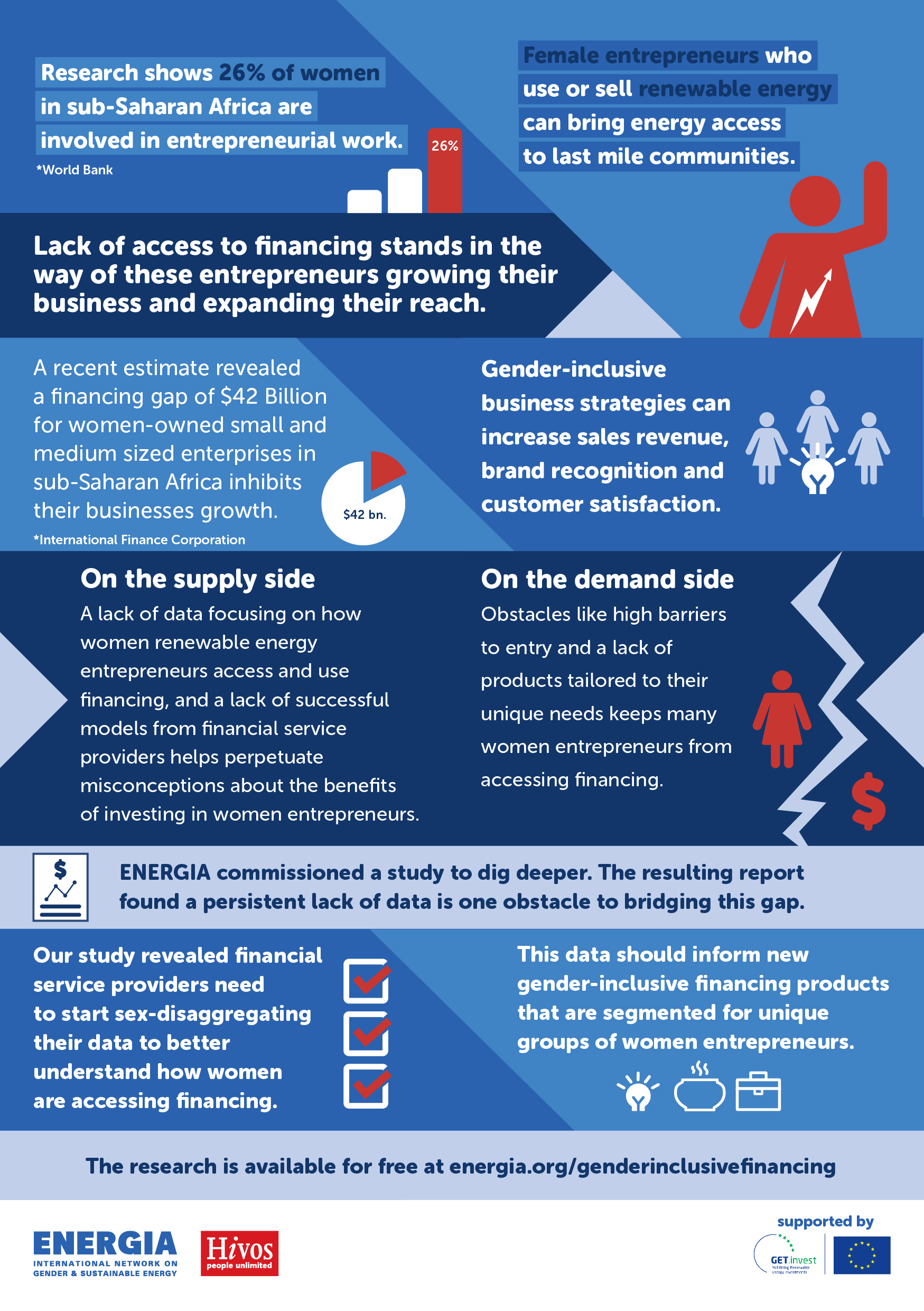

Women entrepreneurs represent one in three growth-oriented entrepreneurs globally, and research from the World Bank shows that 26% of women in Sub-Saharan Africa are involved in entrepreneurial activity—the highest rate in the world. Recent estimates in Sub-Saharan Africa reveal that women-owned and led micro and small enterprises (WMSEs) have a financing gap of $8 billion, while women-owned and led small and medium enterprises (WSMEs) have a financing gap of $42 billion.

ENERGIA, supported by the European programme GET.invest, recently commissioned a report, written in partnership with Distill Inclusion, to collect examples of financing models focused on women-owned or led micro, small, and medium-sized enterprises (WMSMEs), but instead found few examples of sustainable or scalable gender inclusive financing models. Further, they found a lack of data or knowledge about this underserved clientele that would incentivize renewable energy financiers and financial services providers to adopt more inclusive strategies.

Due to this knowledge gap, many financial services providers and renewable energy companies fail to see all the opportunities for increasing investment in women-owned and women-led renewable energy companies. Women are often treated as one singular customer segment within and outside of the renewable energy sector, which means that many providers may be missing the business case for serving certain segments of women entrepreneurs.

For example, anecdotal reports show that female off-grid customers have higher net promoter scores—which measures someone’s willingness to recommend a company’s services or products to others— than men. Additionally, results from a five-year pilot study on how gender inclusive strategies impact business—highlighted in a 2022 report by Shell Foundation and Value for Women —revealed that when businesses adopt gender inclusive strategies, they see increases in sales revenue, customer retention, brand recognition, and customer satisfaction.

When businesses incorporate gender-specific business strategies and acknowledge that women represent many customer segments with distinct energy and financing needs and repayment behaviors, they often see positive results.

Download the full research report.

Here are two strategies that financial service providers have used to serve and meet the distinct needs of their women customers:

Bidhaa Sasa

Many renewable energy technology companies steer clear of customer research because they perceive it to be a prohibitively costly venture, but in actuality, even small companies can successfully and sustainably integrate customer research into their business model. For example, Bidhaa Sasa—a social enterprise offering last-mile finance and distribution services in Kenya and Uganda, whose customer base consists primarily of low-income women without access to land- or cash-based collateral.

Bidhaa Sasa makes a significant effort to research their customers’ needs and preferences and view this research as critical to their success. They collect data on their customers and use this information to refine their product and finance offerings with the end goal of increasing the percentage of women in their customer and loan portfolios.

To meet the needs of this specific segment of women without access to collateral, Bidhaa Sasa changed their financing model to a group liability model and prioritized affordability and repayment plans. In doing so, they have helped many women within this group access solar, cooking, and agricultural technologies for the first time.

The group liability model played a key role in offering affordability and addressing the collateral restraints of their customers. Bidhaa Sasa finances assets for individual women and men, but by positioning them in groups of five, they lower the risk of non-payment and help offer growth opportunities for each group member.

Additionally, through a direct-sales and primarily woman-to-woman distribution model, Bidhaa Sasa leveraged the strong trust within women’s networks and thereby reduced costs associated with marketing and customer acquisition.

Access Bank Nigeria

In order to strengthen its value proposition to women customers, KIT supported Access Bank Nigeria by conducting customer research designed to identify unique female enterprise customer segments in Nigeria. These segments included:

- Career-focused women who do not yet have their own families or their own business.

- Women who are married, have children, and are at varying levels of involvement in the workforce, from non-working women to those who run informal, home-based businesses.

- Women who manage and make financial decisions for their own micro, small, and medium-sized enterprises.

Using these unique segments, the bank tailored and redesigned its offerings to meet the needs of these three different types of women. As part of this, they offered new loans and business account options for women with their own businesses. For women with enterprises who weren’t ready to borrow, they also offered business support services.

Breaking down the customers into different segments helped the bank better understand the needs of an important customer base: WMSMEs. It turned out that the women were interested in loans and financing, but they were actually much more interested in non-financial support. Bundling additional services with the loans led to greater customer uptake. Within three years, the initiative helped grow savings account balances by 46% for women across the three segments and increased lending to WMSMEs by 58%.

Bidhaa Sasa and Access Bank Nigeria illustrate how businesses can employ simple, customer-focused strategies, like conducting customer research and customer segmentation, in order to better design or refine existing product and service offerings. In turn, this can encourage greater uptake by customer segments ranging from low income farmers to women-owned or led small and medium enterprises.

To read the full research report and learn more about what’s needed to create a more inclusive financing ecosystem for WMSME’s working with renewable energy in sub-Saharan Africa click here.